Open Access (OA) is a procurement model where renewable power, such as solar energy, is generated at off-site plants and supplied to corporate consumers through the existing transmission and distribution network. This enables businesses to source large volumes of clean power without installing generation assets at their own premises, while improving cost efficiency and supporting long-term decarbonisation goals.

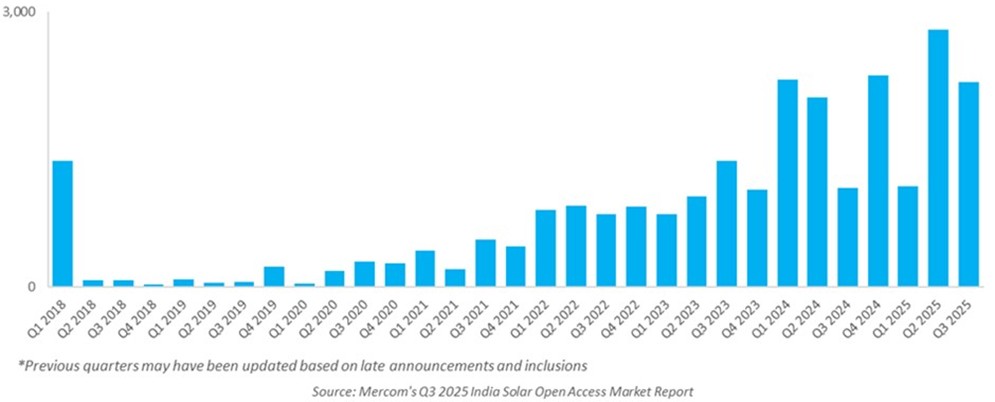

Adoption of solar open access in India has accelerated significantly over the past year. In the first nine months of 2025, the country added more than 6 GW of new solar open access capacity, taking the cumulative base close to 28 GW by September 2025. This represents an approximate 13% year-on-year growth, underlining how open access is rapidly becoming a preferred procurement route for corporates.

FPEL’s 150 MWp Open Access Solar Park in Dhule, Maharashtra

The Government Push Powering Solar Open Access Adoption

India’s renewable transition is being strongly supported by central and state governments through green open access regulations, waiver of inter-state transmission charges, banking facilities, and hybrid plus storage policies.

Key enablers include:

- Green Open Access Rules to simplify approvals.

- Increased focus on hybrid projects and Battery Energy Storage Systems (BESS).

- Financial incentives such as transmission and wheeling charge exemptions.

- Clearer banking and net-metering frameworks.

As a result, India solar open access installations witnessed strong growth in 2025, with certain states clearly leading the adoption curve.

Quarterly installations* of Open Access – Solar (in MW)

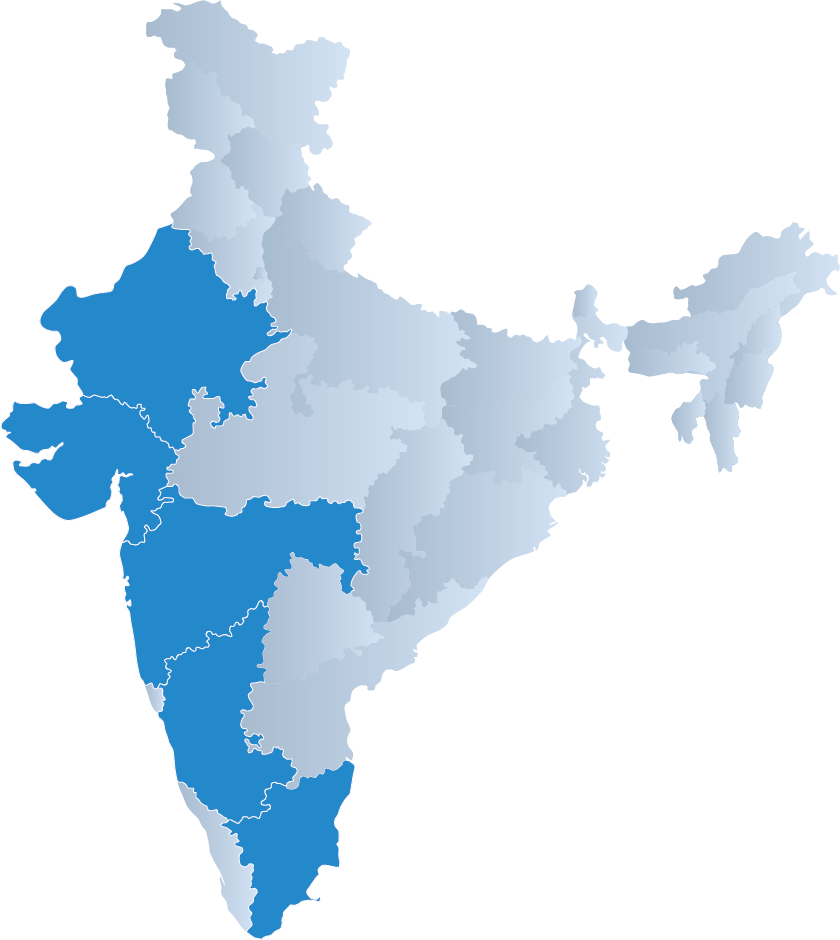

India’s Most Progressive States for Solar Open Access Adoption

Rajasthan – Where India’s Solar Story Truly Amplifies

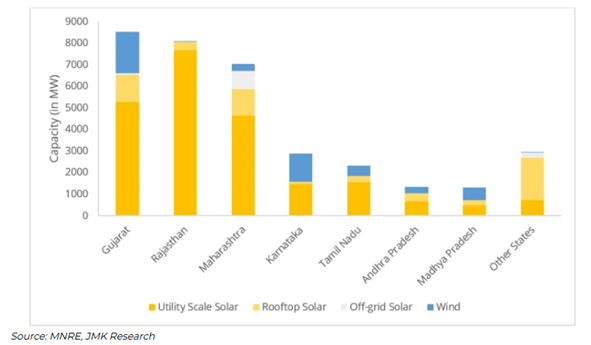

Installed Solar Capacity: 35.9 GW

With more than 325 clear sunny days every year, Rajasthan naturally became India’s solar capital. Today, the state leads the country in installed solar capacity and continues to dominate the open access landscape, contributing around 19% of national OA additions in the first nine months of 2025. Its pipeline is the largest in the country, largely driven by standalone solar projects, while hybrid and solar-plus-storage capacities are also rising steadily. The recently introduced RERC Green Open Access Regulations 2025, along with generous incentives for BESS-integrated projects, have further strengthened Rajasthan’s position as the most attractive destination for solar open access.

Karnataka – The Open Access Trailblazer

Installed Solar Capacity: 10.6 GW

Karnataka was one of the earliest states to open its power markets to open access, and the results are now clearly visible. In the first 9 months of 2025 alone, the state contributed more than a quarter of India’s total solar OA additions, recording an impressive 91% year-on-year growth. Nearly half of Karnataka’s large-scale solar capacity is already under open access, reflecting strong confidence among corporate buyers. With flexible monthly banking provisions and a climate supportive of both solar and wind, Karnataka continues to set the benchmark for renewable procurement in India.

Maharashtra – Flexibility Meets Scale

Installed Solar Capacity: 17.2 GW

Maharashtra’s solar open access growth is being driven by scale, flexibility, and policy clarity. The state accounted for 21% of all open access solar capacity added in first 9 months of 2025, while more than 45% of its installed large-scale solar portfolio now operates under open access. What makes Maharashtra particularly attractive is the ability for corporates to combine rooftop net metering with offsite open access, unlocking multiple saving opportunities from a single energy strategy. This combination has made the state one of the most mature OA markets in the country.

Gujarat – When Rising Tariffs Drive Clean Choices

Installed Solar Capacity: 24.8 GW

In Gujarat, rising electricity tariffs are accelerating the shift to open access solar. With C&I tariffs increasing by up to 9% in FY26, solar open access has become a compelling commercial alternative. The state contributed 10% of India’s total OA additions in 2025, backed by a 28% growth in solar open access capacity. Gujarat’s renewable policy targets a 50% renewable share by 2030, signalling strong long-term commitment to clean power adoption.

Tamil Nadu – Policy-Driven Momentum

Installed Solar Capacity: 11.5 GW

Tamil Nadu’s steady rise in solar open access adoption is being fuelled by enabling regulatory reforms. The state now ranks fifth in cumulative open access capacity, supported by reduced additional surcharge and clear eligibility for industries with connected loads above

50 kW. With banking allowed at an 8% charge, Tamil Nadu is becoming a more attractive state for corporates to procure renewable power through open access.

State-wise solar and wind capacity addition in India from January to September - 2025

FPEL’s 105 MWp Open Access Solar Park in Babina, Uttar Pradesh

Fourth Partner Energy’s Footprint Across India’s Leading Solar Open Access States

Fourth Partner Energy (FPEL) has established a strong open access presence across India’s most progressive renewable energy markets, with several operational assets and a robust pipeline of projects under development. Our footprint across states such as Gujarat, Maharashtra, Karnataka, and Tamil Nadu reflects our commitment to enabling corporates to transition to clean power at scale.

Through these states, FPEL currently serves several leading organisations including TCS, Hatsun Agro, United Breweries, SKF, Hyundai, and many others, helping them achieve sustainability goals while delivering cost savings through reliable solar energy open access solutions.

FPEL’s Solar Parks across these leading states:

| State | Capacity |

|---|---|

| Maharashtra | 680 MWp |

| Gujarat | 78.1 MWp |

| Tamil Nadu | 139 MWp |

| Karnataka | 852.9 MWp |

FPEL’s 75 MWp Open Access Solar Park in Atharga, Karnataka

FPEL’s Pan-India Open Access Footprint

States like Rajasthan, Karnataka, Maharashtra, Gujarat, and Tamil Nadu are clearly leading India’s open access solar revolution, driven by strong policies, infrastructure readiness, and high corporate demand. However, this growth is not limited to just these states. Emerging markets such as Uttar Pradesh, Haryana and Telangana are also amping up their renewable frameworks and are expected to play a major role in the next phase of India’s green power transition.

Want to procure Renewable Energy via Open Access for your business?

Reach out to marketing@fourthpartner.co

Frequently Asked Questions

Who can opt for open access?

Typically, C&I consumers with connected loads above 50 kW or as specified by state regulations.

Is open access cheaper than grid power?

Yes. With rising grid tariffs and policy incentives, OA solar offers significant long-term cost savings up to 50%.

Does open access support Net Zero goals?

Absolutely. It enables companies to directly procure clean energy, accelerating their decarbonisation journey.

How long does it take to commission a solar open access project?

On average, a solar OA project can be commissioned within 3 to 9 months, depending on land availability, approvals, and grid connectivity.

What makes solar open access a smart choice for corporates today?

It helps reduce long-term power costs while enabling businesses to achieve their RE100 targets.

Can solar open access amplify the impact of rooftop solar installations?

Yes. By combining rooftop solar with open access procurement, businesses can significantly increase their renewable energy consumption, maximise clean power usage across facilities, and move faster towards their Net Zero goals.